Rent Control Can Destroy Residential Real Estate Returns

The Future of Rent Stabilization

The future of rent control is inseparably tied to the supply of rental housing nationwide.

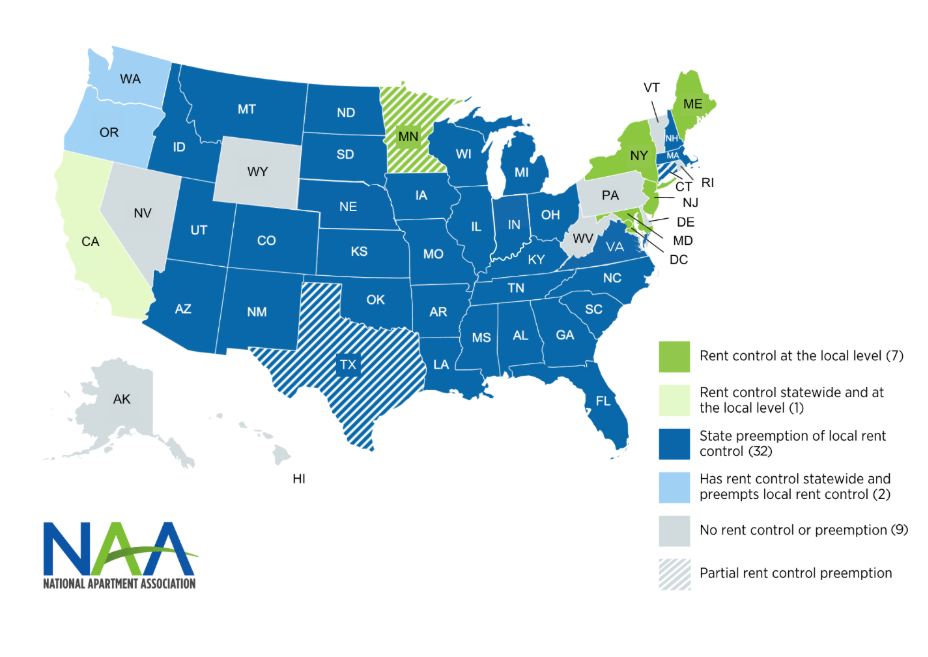

Currently, rent control in the United States is limited to a relatively small number of states and local jurisdictions, but as tenants continue to feel financial pressure, they will keep pushing policymakers to limit rent increases. As of 2026, Washington is the newest state to enact rent-control legislation, while California, Oregon, and several local jurisdictions, including Washington, D.C., continue to operate under rent-control or rent-stabilization regimes.

Figure 1. U.S. Rent Control Map, 2026

States with statewide rent control, local rent control, and states that preempt local rent control.

Policymakers often frame rent control as a tool to slow rent hikes and prevent displacement in high-cost markets. In reality, it often creates the opposite result: less investment, less maintenance, and less housing supply over time.

Major cities such as New York, San Francisco, Los Angeles, Seattle, Portland, and Washington, D.C. continue to maintain some of the strongest rent regulations while also struggling with housing shortages.

Rising Operating Costs

Residential owners are getting squeezed from every direction.

Maintenance costs are rising. Utilities are rising. Insurance is rising. Property taxes are rising. At the same time, many rent-controlled markets restrict the owner’s ability to increase income fast enough to keep pace.

A hidden cost in many states is the difficulty of removing non-paying tenants, especially when delay tactics and extended litigation drag out the process and further erode cash flow.

Supply And Value Effects

Rent control may reduce the supply of rental housing as investors sell.

Research cited by the National Apartment Association shows that rent control primarily affects the regulated stock itself, but the damage does not stop there. In response to lower returns, many owners convert properties to condominiums or sell units outright. In Washington, D.C., for example, the number of rent-controlled units declined from 85,000 in 1984 to about 72,878 in 2020.

The same research notes that rent control can reduce new development, discourage reinvestment, and distort market pricing. In New York City, sale prices of affected multifamily buildings fell by more than 17 percent after universal rent control. In St. Paul, the introduction of rent control in 2021 was associated with a 7% to 13% decline in the value of rent-controlled properties.

St. Paul As A Warning

Saint Paul is a textbook example of what happens when policymakers interfere too aggressively with rental economics.

The city adopted rent stabilization in 2021 with a strict 3% annual cap, then later amended the rules and added exceptions because the original policy was too rigid to function in the real world. That is the predictable result when lawmakers ignore capital needs, rising operating expenses, and investor behavior.

If a policy needs constant repair just to remain workable, it was a flawed policy from the start.

Investor Behavior

The message for investors is simple: capital goes where it is treated well.

When rent control limits the ability to raise income, investors respond by moving money elsewhere. They buy in markets where they can protect margins, maintain properties, and earn an acceptable return. They avoid markets where government policy traps capital and reduces flexibility.

Rental property is not passive. It requires ongoing investment for roofs, paint, paving, repairs, elevators, plumbing, landscaping, and compliance. When rent growth is artificially capped, owners are forced to defer those investments, and the quality of the housing stock declines.

Conclusion

Rent control does not solve housing economics. It distorts them.

For investors, that means lower returns, weaker asset performance, and less flexibility to maintain and improve properties. For the market, it means less supply, less reinvestment, and a steadily deteriorating rental stock. Smart investors should focus on markets where rents can better reflect operating costs, capital needs, and market conditions. In jurisdictions that punish ownership, capital should go elsewhere.

Clifford A. Hockley is Principal Broker at SVN | Bluestone, as well as the managing member of Cliff Hockley Real Estate Consulting, LLC. As a Certified Property Manager & Designated Managing Broker, Cliff has 42 years of experience in the brokerage and management of Real Estate companies. Bluestone and Hockley Real Estate Services managed condominium associations, multi-family, and commercial properties in the greater Portland area. He was focused on running the company and involved with investment property brokerage. He worked with financial institutions, governmental agencies, private investors, and not for profit organizations. He also has vast knowledge in budgeting, organizational management, and building structures. His previous experience includes over five years in accounting, production supervision for a manufacturing company, and work for state agencies in California.

Cliff grew Bluestone and Hockley Real Estate Services into a 100 employee company that managed over 2 billion dollars of real estate assets before he sold the company in 2021. He also supervised a sales team of over 15 real estate brokers for over 35 years. His monthly newsletter, QuickFacts has over 2,300 subscribers. He has been involved in numerous real estate transactions that include industrial, retail, office, and multifamily properties. Cliff has also written a book called “Successful Real Estate Investing; Invest Wisely, Avoid Costly Mistakes and Make Money” published by Morgan James Publishing in 2019.

Cliff has successfully coached real estate investors and CEOs located throughout the United States since 2015. He has acted as a sounding board to help untangle knotty issues that need an experienced outside opinion. He guides leaders who find it is “lonely at the top” and need an experienced hand to help set a strategic direction, sort out operational problems and want to talk through challenging business decisions.

He has served as an adjunct professor at Portland State University from 2028 – 2021, teaching classes in: Intro to Real Estate, Basic Real Estate Finance, Property Management as well as Real Estate Investment Fundamentals. He has instructed hundreds of students and believes that substantial preparation and active student engagement are crucial for learning and appreciating the field of real estate. Students appreciate his candor and real-world experience.

Among his many civic activities, Cliff served on the Board of Directors for the Portland Chapter of the Institute of Real Estate Management (IREM) and the Rental Housing Alliance of Oregon. In 2014 he was recognized by IREM as board member of the year, and in 2015 he earned an achievement award in brokerage from SVN International. In the years 2000 & 2003, he was recognized by IREM as Certified Property Manager of the Year.